http://www.ft.com/cms/s/2/8d0ec4de-9342-11df-96d5-00144feab49a.html

I did not know that you could have been saving at NS&I with 100% gaurantee. Now you can't, unless you already were.

Monday, July 19, 2010

Thursday, June 3, 2010

Study finds that a lack of numerical ability contributed to the subprime mortgage crisis. Poor numerical ability leads to poor financial managements. Gordon brown?

The study linked to below shows that poor numerical skills can partly explain why people defaulted on their subprime mortgages. The result accounts for social background and also the type of mortgage product, so those on the same product was more likely to default if their basic maths was poor. One explanation offered is that people with good basic maths skills are better at planning their finance and possibly being aware that in the good times you must save to prepare for the bad. I remember that Gordon Brown admitted that his maths was not very good. I also remember that Gordon brown spent loads of money when times were good and denied that the bad times would return.

http://abdistri.net/typo/fileadmin/user_upload/0000_named_list/20100515_Financial_Literacy_and_Subprime_Mortgage_Delinquency.pdf

http://abdistri.net/typo/fileadmin/user_upload/0000_named_list/20100515_Financial_Literacy_and_Subprime_Mortgage_Delinquency.pdf

Tuesday, May 18, 2010

UK Inflation; CPI is 3.7% and RPI is 5.3%

Savers are really getting screwed now. Best to spend your money, which sounds silly but it looks like the government likes inflation (we do need to reduce the debt) and government policy is for low interest rates.

One ray of hope, but will only count for a little:

You can get 5% (fixed until 1 June 2011) at northern rock with their ‘fixed rate regular savings account’. you can only put in £250 per month but access is easy

One ray of hope, but will only count for a little:

You can get 5% (fixed until 1 June 2011) at northern rock with their ‘fixed rate regular savings account’. you can only put in £250 per month but access is easy

Monday, May 17, 2010

Coalition Government; Capital Gains tax and cutbacks

The changes to Capital Gains Tax will most likely result in low yield rental properties being sold off. Those who are into the property market long term will probably hold on as long as possible. Perhaps distressed sellers will come from public sector workers, who have second homes as an investment, that will lose out in the next two years, but the real cutbacks will only start next year. Still this (some short term selling off) should give some much needed volume to the market.

Meanwhile the Government keeps up its claim that its policies will keep interest rates down. The prudent will be bailing out the reckless for some time to come I think. Things will likely change next financial year. I expect 1 in 7 public sector workers will lose their jobs, either directly or as a result of lower temporary work, less holiday time, lower and fewer bonuses and a general reduction in other perks. The cutbacks in government spending will affect many lives in 2011/2012. The best advice would be for individuals to save now for those rainy days. Not much incentive to save now though.

Meanwhile the Government keeps up its claim that its policies will keep interest rates down. The prudent will be bailing out the reckless for some time to come I think. Things will likely change next financial year. I expect 1 in 7 public sector workers will lose their jobs, either directly or as a result of lower temporary work, less holiday time, lower and fewer bonuses and a general reduction in other perks. The cutbacks in government spending will affect many lives in 2011/2012. The best advice would be for individuals to save now for those rainy days. Not much incentive to save now though.

Thursday, April 29, 2010

Gordon brown's gaffe

I find it annoying that they keep ignoring the fact that Gillian Duffy was continually making the point about the deficit and how it is going to be repaid. It is like the media wants to ignore this. Savers are paying for it and will continue to do so.

Saturday, April 17, 2010

Tuesday, April 13, 2010

ISA Season

Anyone considering taking out an ISA this year? Around 2.5% can be earned. Some people have mortgages that are below this.

With inflation now well above those ISA rates, it means that you really are paying for almost everything in the economy at the moment as long as you try to save.

With inflation now well above those ISA rates, it means that you really are paying for almost everything in the economy at the moment as long as you try to save.

Wednesday, April 7, 2010

Property confidence back to 2007 levels; Beware

The article linked to below shows that confidence in rising house prices is now at the level it was in 2007. It seems that when the majority believe prices will go up then they go down and when the majority thing prices will go down then they go up (see confidence at the beginning of 2009).

Does this mean that prices are about to go down? I don’t know about that but it does show that you can’t trust surveys on confidence.

http://www.thisismoney.co.uk/mortgages-and-homes/house-prices/article.html?in_article_id=502424&in_page_id=57

Does this mean that prices are about to go down? I don’t know about that but it does show that you can’t trust surveys on confidence.

http://www.thisismoney.co.uk/mortgages-and-homes/house-prices/article.html?in_article_id=502424&in_page_id=57

Tuesday, April 6, 2010

UK General Election 6th May 2010

Your choice on who to vote for but for god’s sake vote. Especially you youngsters.

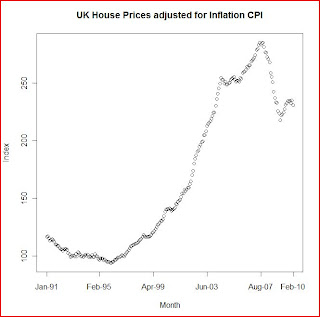

UK House prices. A long term Bear Market?

This article picks up on my point (see previous post) about inflation adjusted house prices.

http://www.telegraph.co.uk/finance/economics/houseprices/7557222/UK-house-prices-face-prolonged-bear-market.html

http://www.telegraph.co.uk/finance/economics/houseprices/7557222/UK-house-prices-face-prolonged-bear-market.html

Tuesday, March 30, 2010

UK Savers Pay for house price increase in March 2010

House prices increased by 0.7% in March 2010 according to the Nationwide. This figure is seasonally adjusted. The actual increase was 1.98%

You might wonder who is paying for these expensive houses in march? Well it’s you, well done. It’s not the owners as they have very low interest rates and inflation is reducing their debt. Nice for them but someone has to pay for that and fortunately there is you. As long as you don’t complain then things will go on like they are.

You might wonder who is paying for these expensive houses in march? Well it’s you, well done. It’s not the owners as they have very low interest rates and inflation is reducing their debt. Nice for them but someone has to pay for that and fortunately there is you. As long as you don’t complain then things will go on like they are.

Monday, March 29, 2010

UK savers petition the government

It’s about time we started protesting.

This is a start

http://petitions.number10.gov.uk/Savingsrate/#detail

but I really think we should go to the next meeting of the bank of England.

This is another website. We need more of this

http://www.saveoursavers.co.uk/

This is a start

http://petitions.number10.gov.uk/Savingsrate/#detail

but I really think we should go to the next meeting of the bank of England.

This is another website. We need more of this

http://www.saveoursavers.co.uk/

Sunday, March 28, 2010

UK House prices; the last two bubbles and Inflation.

As promised, I have got hold of UK house prices since the peak in 1989 and have a plot of raw house prices (Halifax) and inflation adjusted from 1989 to February 2010. The plots are at the foot of this post. Interestingly you can see that house prices have fallen by more this time (21.9%) than in the last crash (14.7%). Incidentally today’s prices are 17.5% below the August 2007 peak.

The last crash resulted in a bounce along the bottom for several years and did not return to it’s 1989 peak until March 1998. More interestingly however, prices adjusted for inflation (CPI) did not return to their peak until February 2002.

It would be unwise to try and predict where prices will go this time. They could bounce along the bottom for a few more years yet, as they did after the last crash. However one thing that we can perhaps be more certain about is that if we adjust for inflation then prices will not return to 2007 levels for a few years longer still.

The last crash resulted in a bounce along the bottom for several years and did not return to it’s 1989 peak until March 1998. More interestingly however, prices adjusted for inflation (CPI) did not return to their peak until February 2002.

It would be unwise to try and predict where prices will go this time. They could bounce along the bottom for a few more years yet, as they did after the last crash. However one thing that we can perhaps be more certain about is that if we adjust for inflation then prices will not return to 2007 levels for a few years longer still.

Friday, March 26, 2010

House prices fall by 0.3% in February (Land Registry). London prices fall 0.45%

Houses prices were down 0.3% in February according to the land Registry. The average number of transactions per month (over September to December 2009) was 63,687 compared to an average of 39,892 for the same period in 2008. So volumes are up, which should be good.

Some might be interested to know that prices in London have shown the first drop since May 2009. Overall prices in London dropped by 0.45%. This was consistent over all property types (Detached, Semi-detached, Terraced, Maisonette/Flat, ALL)

Some might be interested to know that prices in London have shown the first drop since May 2009. Overall prices in London dropped by 0.45%. This was consistent over all property types (Detached, Semi-detached, Terraced, Maisonette/Flat, ALL)

Thursday, March 25, 2010

The Budget; Stamp duty threshold 250,000. THE DETAILS

If you have questions on the new stamp duty relief this Q&A technical note by HM revenue and Customs should cover them:

http://www.hmrc.gov.uk/budget2010/sdlt-qa-tech-1545.pdf

http://www.hmrc.gov.uk/budget2010/sdlt-qa-tech-1545.pdf

Wednesday, March 24, 2010

The Budget; Stamp duty threshold 250,000

The stamp duty holiday last year did not help house prices. See graph in previous post. House prices went up after removing stamp duty at 175,000 last year..

A better idea would be to make the seller pay stamp duty. There would be no loss of income for the government. If you are moving then there is no loss as you would have to pay anyway. First time buyers or those moving up the ladder would benefit and those living in more expensive houses would pay more.

A better idea would be to make the seller pay stamp duty. There would be no loss of income for the government. If you are moving then there is no loss as you would have to pay anyway. First time buyers or those moving up the ladder would benefit and those living in more expensive houses would pay more.

Tuesday, March 23, 2010

UK house prices since 1991 adjusted for Inflation

To add to the previous post here is the data going back to January 1991 (as far back as the nationwide will go). I also have February 2010 data as the inflation figures just came out. See the foot of this post for three house price plots (Unadjusted, Adjusted for CPI, Adjusted for RPI)

It is interesting to note that the unadjusted figures show that house prices were flat right up to around 1996/1997 when they were seen to rise. However after adjusting for inflation it is clear that in real terms prices kept falling and did not start recovering until gone 1999. As we don’t have the data here for 1989 (the peak of the boom at the end of the 80’s) it is not clear here when prices actually returned to peak levels but it is likely to be around 2001. I hope to have an update on this when I get some earlier data.

A note then for the current situation; if you only look at the raw house price index then it seems that prices crashed in 2007/2008 then recovered in spring 2009 and have recently levelled off. However in real terms they are now starting to fall a little.

So perhaps it will be a good while before house prices reach anywhere near the peak of 2007. The effect of inflation is often forgotten when people value their homes and while someone will not go below (say) 300,000 this year they will be happy to sell it for 300,000 in two years. They will of course have paid off some equity in the two years but inflation does help relieve the pain of a drop in prices.

(The house price index was taken from the nationwide (1993=100) and inflation figures were taken from the office for national statistics)

Plot 1; UK House prices since January 1991 (1993 = 100)

Plot 2; UK House prices since January 1991 adjusted for CPI (1993 = 100)

Plot 3; UK House prices since January 1991 adjusted for RPI (not including mortgage interest)

(1993 = 100)

It is interesting to note that the unadjusted figures show that house prices were flat right up to around 1996/1997 when they were seen to rise. However after adjusting for inflation it is clear that in real terms prices kept falling and did not start recovering until gone 1999. As we don’t have the data here for 1989 (the peak of the boom at the end of the 80’s) it is not clear here when prices actually returned to peak levels but it is likely to be around 2001. I hope to have an update on this when I get some earlier data.

A note then for the current situation; if you only look at the raw house price index then it seems that prices crashed in 2007/2008 then recovered in spring 2009 and have recently levelled off. However in real terms they are now starting to fall a little.

So perhaps it will be a good while before house prices reach anywhere near the peak of 2007. The effect of inflation is often forgotten when people value their homes and while someone will not go below (say) 300,000 this year they will be happy to sell it for 300,000 in two years. They will of course have paid off some equity in the two years but inflation does help relieve the pain of a drop in prices.

(The house price index was taken from the nationwide (1993=100) and inflation figures were taken from the office for national statistics)

Plot 1; UK House prices since January 1991 (1993 = 100)

Plot 2; UK House prices since January 1991 adjusted for CPI (1993 = 100)

Plot 3; UK House prices since January 1991 adjusted for RPI (not including mortgage interest)

(1993 = 100)

Monday, March 22, 2010

UK House prices adjusted for Inflation

Below is an interesting look at house prices since the peak (Nationwide index) unadjusted and adjusting for inflation. I have used the RPI as a measure of inflation (Office for national statistics)). The first plot takes the raw data from the nationwide, while the second plot used PRI after taking out mortgage interest payments. . Both plots show that the return to growth of house price in 2009 faded by the end of the summer and has remained flat since. I will update this for the most recent figure (feb 2010) soon.

Sunday, March 21, 2010

Changes to the Lending Code makes promotes excessive borrowing

http://www.independent.co.uk/money/spend-save/simon-read-new-code-shows-lenders-how-to-be-compassionate-1924575.html

I am looking to buy a house at the moment. I can follow two routes:

One way would be to spend within my means, make sure that if interest rates rise I will still be able to pay the mortgage and also making sure that while I pay the mortgage I can still save enough so that if I lose my job I will still be able to pay the mortgage for a couple of months.

But the above article makes me think that would be a mistake. I will spend as much as I can and not worry because if times get hard I will be bailed out by those who were prudent.

I am looking to buy a house at the moment. I can follow two routes:

One way would be to spend within my means, make sure that if interest rates rise I will still be able to pay the mortgage and also making sure that while I pay the mortgage I can still save enough so that if I lose my job I will still be able to pay the mortgage for a couple of months.

But the above article makes me think that would be a mistake. I will spend as much as I can and not worry because if times get hard I will be bailed out by those who were prudent.

Friday, March 19, 2010

Last of Goodwin's RBS directors retires – with £13.5m pension pot

Gordon Pell will receive £582,000 a year after stepping down at the end of the month. He is the last of the Fred goodwin era and as a retiring director of the Royal Bank of Scotland will receive a £13.5m pension pot.

A little about this guys talent:

He was formerly group director of Lloyds TSB UK Retail Banking before joining National Westminster Bank Plc as a director in February 2000 and then becoming Chief Executive. He was also a member of the FSA Practitioner Panel and deputy Chairman of the Board of the British Bankers Association in September 2007.

What a great track record of poor performing banks (OK Nat West, not too bad. Smaller and easier than RBD and Lloyds though) and agencies. Well worth the money. You are paying for it.

A little about this guys talent:

He was formerly group director of Lloyds TSB UK Retail Banking before joining National Westminster Bank Plc as a director in February 2000 and then becoming Chief Executive. He was also a member of the FSA Practitioner Panel and deputy Chairman of the Board of the British Bankers Association in September 2007.

What a great track record of poor performing banks (OK Nat West, not too bad. Smaller and easier than RBD and Lloyds though) and agencies. Well worth the money. You are paying for it.

Thursday, March 18, 2010

Budget 2010: You are the Chancellor. What would you do?

If I were him I would keep screwing savers and those who have nothing (the next generation and current youngsters) to bail out those who overspent in the past.

However if I were me in his job I would reward people who make the right decisions, not the ones who make the wrong ones.

However if I were me in his job I would reward people who make the right decisions, not the ones who make the wrong ones.

Adair Turner's report; home loans should be less easily available. More prudence.

http://www.guardian.co.uk/business/2010/mar/17/adair-turner-make-home-loans-less-available-larry-elliott

The end of this article has some truth “Rising house prices simply transfer wealth from young people to their parents.” However more generally at the moment, low interest rates and rising house prices are transferring wealth from those who were prudent to those who were reckless

The end of this article has some truth “Rising house prices simply transfer wealth from young people to their parents.” However more generally at the moment, low interest rates and rising house prices are transferring wealth from those who were prudent to those who were reckless

Wednesday, March 17, 2010

Bank of England unanimous on interest rate freeze. Shall we start complaining?

All nine members voted for no change, even though inflation is currently at 3.5%, well above the 2% target. The MPC was also unanimous in keeping the £200bn quantitative easing (QE) programme unchanged.

It does not look like they worry about the fact that inflation is above savings rates. The notes of the meeting said inflation was set to remain above the 2% target for some months to come, and that there were certain risks from the weak pound which has now fallen in value by 25% since 2007. So they care less about inflation and care even less about savers.

How about a demonstration at the next Bank of England meeting? 7th April.

It does not look like they worry about the fact that inflation is above savings rates. The notes of the meeting said inflation was set to remain above the 2% target for some months to come, and that there were certain risks from the weak pound which has now fallen in value by 25% since 2007. So they care less about inflation and care even less about savers.

How about a demonstration at the next Bank of England meeting? 7th April.

Tuesday, March 16, 2010

Government rejects EU call to cut deficit faster

A government that thinks it knows more than the market is dangerous. It is a fair argument that things should have been better regulated over the last few years but now we have a monster. There is no point in trying to make a decision about your future (should I buy a house, should I save (interest rates are below inflation), should I invest in shares, should I accept that job?) because most things economic now depend on government decisions which means you need to second guess the government, make friends with the government or (I hope we don’t get there) bribe the government. The government should be a referee for the system not a playmaker.

Monday, March 15, 2010

Buy-to-let tax break plan attacked as further blow to first-time buyers

Stories like this can easily be missed so i bring it to your attention.

http://www.guardian.co.uk/business/2010/mar/15/first-time-buyers-priced-out

Will this make it easier for landlords to extend their portfolios? Lower costs always help.

It is interesting to note that Britons entry into the Forbes richest list was a man who inherited his fortune and makes money from rent. America has people who made their money themselves from very competitive industries (computers and the internet).

Rank 45

http://www.forbes.com/lists/2010/10/billionaires-2010_The-Worlds-Billionaires_Rank_2.html

http://www.guardian.co.uk/business/2010/mar/15/first-time-buyers-priced-out

Will this make it easier for landlords to extend their portfolios? Lower costs always help.

It is interesting to note that Britons entry into the Forbes richest list was a man who inherited his fortune and makes money from rent. America has people who made their money themselves from very competitive industries (computers and the internet).

Rank 45

http://www.forbes.com/lists/2010/10/billionaires-2010_The-Worlds-Billionaires_Rank_2.html

Friday, March 12, 2010

The housing market Feb 2010. Broken.

Nationwide house price index since September (unadjusted)

Sep 09 - 322.8

Oct 09 - 323.2

Nov 09 - 324.7

Dec 09 - 323.4

Jan 10 - 326.1

Feb 10 - 321.8

So it is clear that prices have not moved since september. The bounce of 2009 started in March (feb index = 294.7) and ended in september. It loooks like January and Feb 2010 cancel each other.

A point for reference is that the peak was 368.5 in September 2007. The index now is 12.7% below this,

House prices did not recover that much last year (except for 2 million + houses in central london)

The problem at the moment is that there is no market as sellers are protected by low interest rates and are still under the illusion that houses are worth 2007 prices.

It is very hard to sell or buy a house. This point is missed by the press and government.

Sep 09 - 322.8

Oct 09 - 323.2

Nov 09 - 324.7

Dec 09 - 323.4

Jan 10 - 326.1

Feb 10 - 321.8

So it is clear that prices have not moved since september. The bounce of 2009 started in March (feb index = 294.7) and ended in september. It loooks like January and Feb 2010 cancel each other.

A point for reference is that the peak was 368.5 in September 2007. The index now is 12.7% below this,

House prices did not recover that much last year (except for 2 million + houses in central london)

The problem at the moment is that there is no market as sellers are protected by low interest rates and are still under the illusion that houses are worth 2007 prices.

It is very hard to sell or buy a house. This point is missed by the press and government.

Wednesday, March 10, 2010

UK Youth Rebel

The argument that the massive ‘bail out’ was necessary to save the whole financial system and therefore “all of us” is wearing thin. The only people who have been bailed out are those with assets, large savings and those who rely on pension’s funds and insurance policies dependant on the stock market.

Since the bail out, the value of houses has risen as has the stock market. Those with money, assets and pension funds have been saved. Those who did not have lots of money, assets or pensions will be paying for this for years to come. Generally these people are under 30. They will almost definitely not receive a pension. If house prices keep rising they will probably never own their own home and with interest rates lower than inflation they will never really be able to save any money.

The youth today should not vote Labour or Conservative. They should rebel and force both parties from power.

Since the bail out, the value of houses has risen as has the stock market. Those with money, assets and pension funds have been saved. Those who did not have lots of money, assets or pensions will be paying for this for years to come. Generally these people are under 30. They will almost definitely not receive a pension. If house prices keep rising they will probably never own their own home and with interest rates lower than inflation they will never really be able to save any money.

The youth today should not vote Labour or Conservative. They should rebel and force both parties from power.

Northern Rock: more than 4% of mortgage customers are in arrears

Northern rock needs house prices to go up by 10% to 15% to be saved.

The current government policy seems to be to bail out those who borrowed too much. With inflation at around 4% and interest rates on saving at around 2.5%, sensible people really are paying for those who spent too much and can’t afford to pay it back.

Negative returns on savings with rising house prices punishes people who make the right decisions.

Savers revolt

The current government policy seems to be to bail out those who borrowed too much. With inflation at around 4% and interest rates on saving at around 2.5%, sensible people really are paying for those who spent too much and can’t afford to pay it back.

Negative returns on savings with rising house prices punishes people who make the right decisions.

Savers revolt

Tuesday, March 9, 2010

January trade deficit widens as exports fall

A weaker pound makes UK goods cheaper, but not necessarily more attractive. Quality is another factor as is the ability to guarantee supply.

I guess there is not enough confidence in the UK from international markets, probably because we have a government that does not believe in markets.

I guess there is not enough confidence in the UK from international markets, probably because we have a government that does not believe in markets.

Saturday, March 6, 2010

Buy-to-let king and queen dismantle property portfolio

The argument that we had to bail out the banks, reduce interest rates and start quantitative easing or it would be the end of the world is wearing thin.

Low interest rates and quantitative easing has bailed out those who made mistakes and those who were sensible are paying for it. This article (1) backs up this point with Fergus admitting that the low interest rate has kept them going. These low rates come as a cost to the next generation and those who are not in debt.

1 http://www.guardian.co.uk/money/2010/mar/06/buy-to-let-fergus-judith-wilson?showallcomments=true#end-of-comments

Low interest rates and quantitative easing has bailed out those who made mistakes and those who were sensible are paying for it. This article (1) backs up this point with Fergus admitting that the low interest rate has kept them going. These low rates come as a cost to the next generation and those who are not in debt.

1 http://www.guardian.co.uk/money/2010/mar/06/buy-to-let-fergus-judith-wilson?showallcomments=true#end-of-comments

Friday, February 26, 2010

UK House prices (Nationwide; February 2010 down 1%)

When I look at the data from the nationwide the figure for February is actually a drop of 1.3%. The 1% drop is seasonally adjusted.

Also, they say that the 3 month movement is +1.6% but this is also seasonally adjusted. The actual 3 month movement is -0.9%.

Prices are perhaps going down (slightly), and have been since September. Since September 2009 prices have shown very low rises and falls, overall house prices for this period have fallen 0.3%.

http://www.nationwide.co.uk/hpi/historical.htm

Also, they say that the 3 month movement is +1.6% but this is also seasonally adjusted. The actual 3 month movement is -0.9%.

Prices are perhaps going down (slightly), and have been since September. Since September 2009 prices have shown very low rises and falls, overall house prices for this period have fallen 0.3%.

http://www.nationwide.co.uk/hpi/historical.htm

Thursday, February 25, 2010

UK Growth for 4th quarter 2009

It's a big argument about an estimate that clearly shows there is no growth (plus or minus an error). The most annoying thing about this recession is that reckless businesses and reckless individuals are being bailed out by those who were not reckless. Not a good policy for the long term strength of a country.

Growth or no growth, we should be investing in quality.

Growth or no growth, we should be investing in quality.

Wednesday, February 24, 2010

RBS and LLOYDS performances

One of the main problems here is the belief that a government can run a business, let alone make a ?profit?. RBS and Lloyds will probably never fully pay back the amounts they relied on during the bail out. More likely they will be sold off by a conservative government for a ?loss? and the market will deal with it. I imagine that in 10 years time the biggest UK banks will be Barclays and HSBC. They should be as they have been run well and should be rewarded for that.

In answer to the question 'who is to blame and who is really being bailed out?'

Low interest rates are largely bailing out those who overspent and those who did not are paying for it.

In answer to the question 'who is to blame and who is really being bailed out?'

Low interest rates are largely bailing out those who overspent and those who did not are paying for it.

Wednesday, February 17, 2010

UK Savers Revolt

Most people seem to assume that savers are only bailing out the banks. It is true that the banks have been bailed out, however at the moment savers are generally bailing out the people who borrowed heavily in the last few years and cannot afford to pay it back. There should be more political angst against those who remortgaged on the increase in the value of their house (which is unearned income) and are now being protected by low interest rates. Do you want to live in a country that helps those who were foolish and punishes those who were not? With inflation above 4% (when you account for costs associated with homes, with or without a mortgage) then the money you have is going down in value even with interest. The low interest rates are protecting those who made a mistake and the reduced value of your money is paying for it.

You do not have to pay for others mistakes. It would be better to take you money out of its current savings account and move it to the highest possible rate you can find, which probably won’t be in the accounts run by the banks who are servicing these cheap mortgages. Better still would be to Just REVOLT. Take you money out. Move it abroad if you can. If you can’t, then make a run on one bank and move the money to another. Do whatever it takes to put pressure on the banks and government to give a reasonable savings rate and to stop supporting those who caused the financial problems.

Make no mistake; the banks and reckless spenders need your money. Don’t let them have it without a fight.

You do not have to pay for others mistakes. It would be better to take you money out of its current savings account and move it to the highest possible rate you can find, which probably won’t be in the accounts run by the banks who are servicing these cheap mortgages. Better still would be to Just REVOLT. Take you money out. Move it abroad if you can. If you can’t, then make a run on one bank and move the money to another. Do whatever it takes to put pressure on the banks and government to give a reasonable savings rate and to stop supporting those who caused the financial problems.

Make no mistake; the banks and reckless spenders need your money. Don’t let them have it without a fight.

Subscribe to:

Posts (Atom)